Why the shift to Financial Infrastructure as Code is no longer optional.

In 2021, a misconfigured payment routing rule at a major digital bank locked thousands of customers out of their accounts for 19 hours. The root cause wasn't a cyberattack, a data breach, or a failed hardware component. It was a manually applied change, undocumented, unreviewed, and impossible to roll back cleanly.

The institution had some of the most sophisticated transaction processing in the world. But the rule that governed how payments were routed lived in a database table, maintained by hand.

When a single manual configuration can bring a digital bank to its knees, the question isn't whether to change your approach it's how quickly you can.

Modern financial platforms are expected to process thousands of transactions per second across borders, currencies, and regulatory regimes while operating with near-perfect reliability, complying with Basel III, PCI DSS, and SOX, and adapting to markets that change faster than annual audit cycles. At the same time, they face accelerating pressure from embedded finance, open banking, real-time payment rails, and AI-driven personalization.

Many organizations are meeting these demands with systems that were never designed for them: manual configurations, fragmented controls, siloed governance, and architectures where compliance is retrofitted rather than built in.

There is a better model. It's called Financial Infrastructure as Code, and it's redefining how leading FinTech platforms are built, governed, and scaled.

From 'Configure It' to 'Code It'

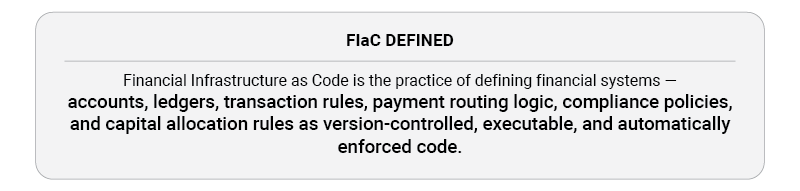

Infrastructure as Code, where servers, networks, and cloud resources are defined in version-controlled, machine-readable files rather than managed through UI consoles, transformed software engineering over the last decade. Financial Infrastructure as Code (FIaC) applies that same discipline to the financial layer itself.

Under FIaC, every layer of the financial platform becomes declarative and reproducible. Account structures, transaction posting rules, UPI limits, AML thresholds, API authentication policies all written in code, stored in version control, tested in CI/CD pipelines, and deployed the same way software is deployed.

The shift in operating model is elegantly simple: from 'configure it through a dashboard' to 'code it, review it, and deploy it.'

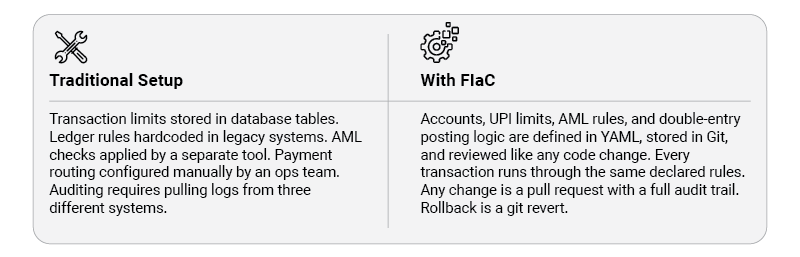

What This Looks Like in Practice

Consider a customer sending ₹1,000 via a mobile banking app.

The result isn't just cleaner architecture. It's a platform where behavior is predictable, auditable, and reproducible, with properties that are non-negotiable at scale.

From Monolithic Products to Programmable Capabilities

The traditional model for financial product delivery was tightly coupled: a lending product bundled origination, underwriting, disbursement, and collections into one system. Changing any single element meant touching everything.

FIaC enables a fundamentally different model, one built around well-defined, reusable API primitives. A 'check-customer-risk' service can be called by any partner application before onboarding a customer, returning a credit score, and required actions. A payment routing module can be configured differently for different geographies by changing a few lines of code. A fee calculation rule can be overridden for a specific partner tier without touching the core platform.

This composability is what makes embedded finance, FinTech marketplace models, and white-label banking commercially viable. The old model was: buy a product, configure it through a UI. The new model is API-Driven Finance; compose capabilities through APIs and own the business logic yourself.

The implications for speed of innovation, regulatory agility, and go-to-market timelines are profound.

Compliance Built In, Not Bolted On

In legacy environments, compliance was an afterthought. Systems were built first and governed retroactively. Audits happened quarterly. Security tooling was maintained by a separate team on a separate timeline.

That model doesn't hold up when regulatory changes arrive faster than audit cycles, and when the cost of a single compliance gap can be existential.

FIaC introduces three interlocking practices that eliminate the gap between engineering velocity and governance:

- Compliance-as-Code (CaC); regulatory requirements and risk thresholds expressed as testable, version-controlled rules that run automatically on every deployment.

- Security-as-Code (SaC); security controls such as encryption requirements, API authentication policies, and access rules defined in code and enforced by the build pipeline, not by manual review.

- Policy-as-Code (PaC); infrastructure constraints ('all databases must be encrypted', 'no public S3 buckets', 'all APIs must use HTTPS') enforced by tools like Open Policy Agent or Terraform Sentinel before any resource is provisioned.

Together, these three practices deliver a critical shift in how financial platforms think about governance: security and compliance become properties of the platform itself, not responsibilities delegated to individuals.

In a code-defined system, the rule either passes or it doesn't. There is no ambiguity, no manual interpretation, no gap between policy documents and what the system actually does.

Composability, Resilience, and Scale by Design

As financial platforms operate in increasingly dynamic, high-volume environments, the architecture must allow discrete, autonomous components to be deployed, scaled, and replaced independently without propagating risk across the system.

Under FIaC, each component owns its own boundary. A payment processing module can be scaled horizontally during peak transaction periods without touching the ledger or the fraud detection service. A component that fails degrades gracefully; the rest of the system continues operating. Fault isolation is structural, not incidental.

Dynamic orchestration adds elasticity: resources scale up or down automatically in response to transaction volumes and market conditions, so that growth is absorbed by infrastructure rather than by engineering teams scrambling to re-architect under pressure.

The deeper principle is this: composability, resilience, and scale are not independent design goals; they compound. Reusable components earn trust only when they are resilient. Resilient systems are worth scaling only when they are composable enough to meet new demands without becoming new liabilities.

What FIaC Demands of FinTech Leadership

FIaC is not purely a technical decision. It necessitates a fundamental change in how leadership thinks about technology investment, organizational structure, and talent.

- Engineering-led culture; cross-functional teams co-own technology delivery. Product, risk, compliance, and engineering work from the same codebase, not separate silos.

- Platform thinking; the investment thesis shifts from maintaining systems to building reusable capabilities that other teams and partners can build on.

- Governance at the speed of engineering; compliance and security tooling is embedded into CI/CD pipelines, not added as a gate after delivery.

- Talent strategy; roles evolve from system maintenance to cloud-native architecture, developer experience, and systems thinking.

Organizations that make these investments early will set the pace. Those who defer will spend the next cycle catching up, a significantly more expensive position to be in when regulatory environments tighten and competitive pressure intensifies.

How Cybage Enables the Transition

Cybage has been a technology engineering partner to global FinTech platforms, payment processors, and financial institutions for over two decades. Our work in this space is grounded in one principle: lasting competitive advantage in financial services is built on engineering quality, not feature velocity.

Our FIaC-aligned engineering practice focuses on four capability areas that matter most to financial platform modernization:

- Cloud-native, microservices-based architecture; designing platforms where financial capabilities are discrete, independently deployable services with clear ownership boundaries.

- Infrastructure and operations automation; eliminating manual configuration risk through fintech automation solutions that fully automate infrastructure provisioning, deployment, and platform operations.

- Data-centric system design; treating data as a first-class engineering concern, enabling real-time analytics, event-driven architectures, and AI-ready data infrastructure.

- Large-scale automated validation; building validation platforms that test financial logic, regulatory compliance, and system behavior at the speed of continuous delivery.

The platforms we help build are designed to be scalable, resilient, and compliant by design, not by exception. For clients in complex regulatory environments or undergoing cloud migration, this engineering foundation is the difference between a platform that scales confidently and one that accumulates technical and compliance debt with every release.

The Future Is Code-Defined Finance

Financial Infrastructure as Code represents a fundamental shift in how financial systems are built, governed, and evolved. The organizations that embrace it early will operate with greater speed, lower risk, and stronger trust with regulators and customers alike.

Code, in this model, is not just how the system is built. It is the foundation of trust.

Talk to Cybage

If you are evaluating platform modernization, a cloud migration, or a compliance automation program, we would welcome a conversation about how FIaC principles can accelerate your roadmap. Reach out to our FinTech practice team to explore what's possible.